You've found your dream property in Wadi Al Safa 7. Down payment ready. Stable job. You apply confidently.

Then rejection hits. Not your credit score—it's DBR (Debt Burden Ratio).

In 2026, as Dubai's property market matures, banks strictly enforce UAE Central Bank regulations. Understanding your Debt-to-Income ratio is the mathematical gatekeeper between you and your title deed.

Here's your definitive guide to mastering DBR and securing mortgage approval.

What Is Debt-to-Income Ratio in the UAE?

In UAE banking, DTI is called the Debt Burden Ratio (DBR).

Simply: the percentage of gross monthly income allocated to debt repayments. The Central Bank uses this to prevent over-leveraging.

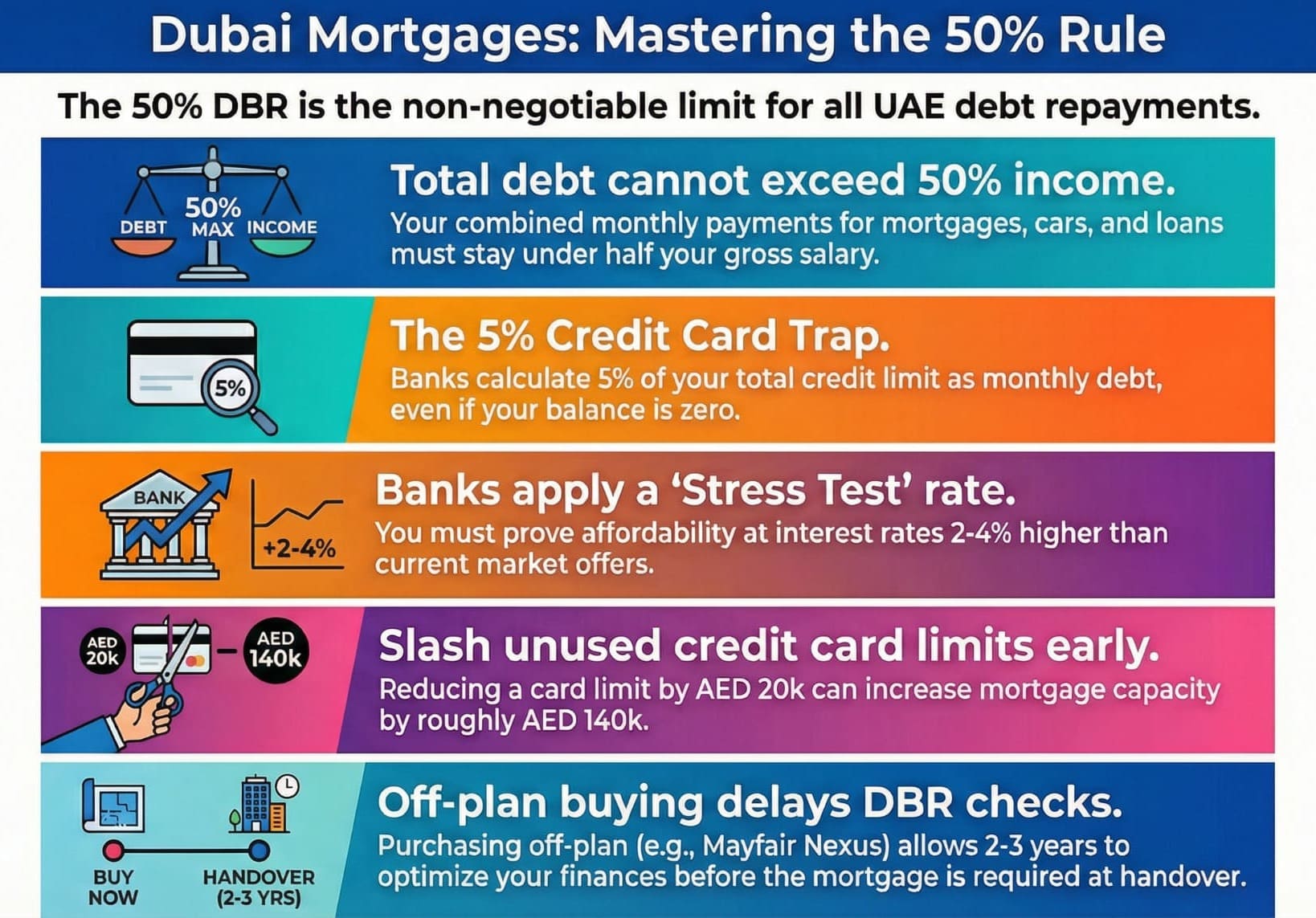

The Golden Rule: 50% Cap

You cannot spend more than 50% of monthly income on debt repayments.

Example:

- Salary: AED 30,000/month

- Maximum debt allowed: AED 15,000/month

- Loan pushing you to AED 15,001 = Automatic rejection

This applies to mortgages, car loans, personal loans, and credit cards.

How Banks Calculate Your DBR

Most buyers calculate incorrectly—they only count debts they actively pay. Banks calculate debts you're liable for.

UAE Bank DBR Formula:

DBR = (Mortgage + Car Loans + Personal Loans + Credit Card Liability) ÷ Gross Monthly Income × 100

Must not exceed 50%

The Stress Test Trap

Banks don't use today's interest rate (e.g., 4.5%). They apply a Stress Test Rate.

The Rule: Calculate affordability assuming rates rise 2-4%.

Impact: Even if you afford the mortgage today, if the stress test pushes DBR over 50%, you're denied.

The Hidden Trap: Credit Card Limits

Where 90% of Dubai buyers fail.

You think: "I pay cards in full monthly—zero debt."

Wrong.

Banks calculate DBR based on credit card limit, not balance.

The 5% Rule

Banks factor 5% of total credit card limit as monthly debt.

Example:

Your Situation:

- Salary: AED 40,000

- Credit Cards: AED 100,000 combined limit

- Current Balance: AED 0 (paid in full)

Bank's Calculation:

- Credit card "debt": AED 5,000/month (5% of 100K)

- Lost mortgage capacity: ~AED 700,000

That unused Emirates card for lounge access? It just cost you a bedroom.

Why This Matters for Mayfair Nexus Investors

For Wadi Al Safa 7 buyers, understanding DBR is crucial for timing.

The Off-Plan Advantage

No Immediate Mortgage: Buying Mayfair Nexus on 70/30 payment plan = pay developer during construction. Doesn't appear as "debt" on credit bureau.

Strategic Delay: Mortgage needed only at handover (Q4 2028). Gives you 2-3 years to:

- Clear car loans

- Reduce credit card limits

- Consolidate debts

- Optimize DBR

Result: Secure asset now, perfect finances later, get mortgage approved at handover.

How to Optimize Your DBR (3-6 Months Before)

1. Slash Credit Card Limits

Action: Reduce limits to actual usage + 20% buffer.

- AED 50K limit, AED 5K spending → Reduce to AED 10K

- Impact: Every AED 20K reduced = AED 1,000/month freed = ~AED 140K additional mortgage capacity

2. Consolidate Liabilities

Before: Car loan (AED 2K) + 2 personal loans (AED 2.5K) = AED 4.5K/month

After: Single consolidated loan = AED 3.2K/month

Savings: AED 1.3K/month = ~AED 180K more borrowing power

3. Optimize Income Structure

Banks count:

- 100%: Basic salary + housing allowance

- 50-70%: Commissions/bonuses

- 0%: One-time bonuses

Strategy: Negotiate higher base salary vs. commission before applying.

4. Close Buy-Now-Pay-Later

Tabby, Tamara now appear on credit reports. Clear 90 days before application.

Interest Rate Environment 2026

Current UAE rates: 4.2-5.5% (down from 5.5-6.5% in 2024)

Lower Rates = Better DBR:

That AED 1,130 saving = ~AED 160K additional capacity at the same DBR.

Refinancing Opportunity: Existing homeowners can refinance to free DBR for second investments.

Strategic Timeline Example

Young professional with tight DBR wants Mayfair Nexus:

Result: Property initially unaffordable → secured through strategic timing.

The Bottom Line

The 50% Debt Burden Ratio is your gatekeeper, but strategic buyers gain advantages:

Key Takeaways:

- Credit card limits destroy mortgage capacity

- Stress tests add 2-4% to calculations

- Off-plan buys delay DBR checks 2-3 years

- 2026 lower rates increase capacity

Your Action Plan:

Immediate:

- Calculate current DBR

- List all credit card limits

- Identify unused cards

This Month:

- Reduce credit limits to usage + 20%

- Cancel unused cards

- Get AECB credit report

3-6 Months:

- Pay off smallest loans first

- Consolidate remaining debts

- Clear BNPL accounts

Strategic:

- Consider off-plan for flexibility

- Research Mayfair Nexus 70/30 plan

- Speak with mortgage brokers

The Mayfair Nexus Solution

Not mortgage-ready today? Mayfair Nexus offers:

- 70/30 Payment Plan - Only 30% at handover (2028)

- No immediate mortgage - Pay developer during construction

- 2-3 year optimization - Perfect DBR while property appreciates

- Wadi Al Safa 7 - Supply-constrained premium location

- Metro timing - Blue Line opens 2029

Lock today's prices. Qualify for tomorrow's mortgage.

Don't Let Math Block Your Dream

The 50% Rule protects you from over-leveraging—but within it, prepared buyers win.

Understanding the system = Better planning = Higher approval rates.

FAQs

Q 1: What is the maximum debt-to-income ratio allowed for UAE mortgages?

A: The UAE Central Bank mandates a maximum Debt Burden Ratio (DBR) of 50% of gross monthly income. This means total monthly debt repayments—including mortgage, car loans, personal loans, and 5% of total credit card limits—cannot exceed half your salary. For retirees, the cap is typically lower at 35%. Exceeding this 50% threshold is the leading cause of mortgage application rejection in Dubai, regardless of credit score or down payment size.

Q 2: How do credit cards affect mortgage eligibility in Dubai?

A: UAE banks calculate 5% of your total credit card limit (not current balance) as monthly debt obligation. An unused AED 100,000 credit limit adds AED 5,000 to your monthly debt calculation, reducing mortgage eligibility by approximately AED 700,000. This applies even if you pay cards in full monthly. The solution: reduce credit card limits to actual usage levels or cancel unused cards 3-6 months before mortgage application to maximize borrowing power.

Q 3: What is the mortgage stress test in the UAE?

A: The UAE mortgage stress test requires banks to verify affordability if interest rates rise. Banks add 2-4% to current rates when calculating your maximum loan amount. If current rates are 4.5%, banks test affordability at 6.5-8.5%. If this higher rate pushes your DBR above 50%, your loan amount is reduced or rejected. This protects borrowers from future payment shock but significantly impacts current borrowing capacity.

Q 4: Can I get a Dubai mortgage with AED 15,000 salary?

A: Yes, several UAE banks offer mortgages to residents earning AED 10,000-15,000 monthly, though borrowing power is severely limited by the 50% DBR rule. With AED 15,000 salary, maximum monthly debt payments allowed are AED 7,500. After deducting existing loans and credit card liabilities (5% of limits), remaining capacity determines mortgage amount—typically AED 800K-1.2M depending on interest rates and other obligations. Target affordable properties in emerging areas like Wadi Al Safa 7.

Q 5: How can I quickly improve my debt-to-income ratio for mortgage approval?

Answer: The fastest DBR improvements:

1. Reduce credit card limits: Every AED 20,000 reduction frees AED 1,000/month (~AED 140K mortgage capacity) 2. Pay off small loans: Eliminate monthly installments completely 3. Consolidate debts: Multiple loans → one lower monthly payment 4. Cancel Buy-Now-Pay-Later: Tabby/Tamara now appear on credit reports 5. Restructure income: Maximize base salary vs commissions

Implement these 3-6 months before application for maximum impact.

Q 6: Does the 50% DBR rule apply to off-plan property purchases?

A: The 50% DBR rule applies when taking a mortgage, not during off-plan developer payment plans. When buying Mayfair Nexus on a 70/30 plan, construction-phase payments to developers typically don't appear as "debt" on Al Etihad Credit Bureau reports. DBR checks occur only when applying for the final mortgage at handover (e.g., final 30-50%). This creates a strategic advantage: secure property today, optimize DBR during construction (2-3 years), then apply for a mortgage with improved financial profile.

Q 7: What income do UAE banks count for mortgage calculations?

A: UAE banks typically count:

100% of:

- Basic salary

- Housing allowance

- Transportation allowance (if guaranteed)

50-70% of:

- Average commissions (last 6-12 months)

- Variable bonuses

- Overtime (if consistent)

Not counted:

- One-time bonuses

- Stock options

- Irregular income

To maximize borrowing power, structure employment contracts with higher base salary rather than commission-heavy arrangements. Banks prefer predictable, guaranteed income streams for DBR calculations.

Q 8: How much can I borrow with AED 30,000 monthly salary in Dubai?

A: With AED 30,000 salary and assuming:

- Zero existing debts

- Zero credit card limits

- 4.5% interest rate

- 25-year term

- 50% DBR limit (AED 15,000 max monthly payment)

- Minus stress test (calculated at ~6.5%)

Approximate borrowing capacity: AED 1.8M - 2.1M

However, existing debts dramatically reduce this. AED 5,000 in existing monthly obligations (loans + 5% of credit card limits) reduces mortgage capacity to ~AED 1.2M-1.5M. Always calculate existing liabilities first.

Q 9: Should I buy off-plan or ready property if my DBR is tight?

A: If DBR is tight (close to 50%), off-plan properties offer strategic advantage. Developer payment plans during construction (e.g., Mayfair Nexus 70/30) don't require immediate mortgage or trigger DBR checks. This provides 2-3 years to:

- Clear existing loans

- Reduce credit card limits

- Increase salary

- Lower interest rate environment

By handover, your DBR improves significantly. Ready properties require immediate mortgage approval with current DBR constraints—potentially blocking purchase entirely.

Q 10: What happens if I exceed the 50% debt-to-income ratio in UAE?

A: Exceeding 50% DBR results in:

- Automatic loan rejection by banks

- Reduced loan amount offered (less than requested)

- Higher interest rates (risk premium)

- Shorter loan tenure (increasing monthly payments further)

Banks cannot override Central Bank regulations. The only solutions: reduce existing debts, increase income, make larger down payment (reducing loan needed), or delay application while improving financial profile. There are no exceptions or workarounds.